After looking into all those research reports on 2012 market outlook by local securities or research houses, it's time for foreign research houses. In this series of 2012 outlook, we kick start with Credit Suisse's report, in which a section of it was written specifically on Malaysia. And, below is the excerpt from it.

Malaysia’s GDP growth to outperform its regional peers'?

Real GDP growth expanded 5.8% yoy in Q3, led by strong private consumption (7.4% yoy) and fixed investment (6.1% yoy), and a surge in government consumption (21.8% yoy). On a seasonally adjusted basis, we estimate that GDP expanded 4.6% qoq annualized in Q3, stronger than that of Korea, Thailand, Singapore, the Philippines, Hong Kong, and Taiwan. Malaysia remains highly exposed to a sharp slowdown in the developed world, but, on a relative basis, we think its domestic demand will hold up better than that of the other small open economies in the region. We expect private consumption growth to remain robust, partly due to high palm oil prices. In addition, fiscal spending from the government should continue to help boost spending in the next few quarters. We think there is upside risk to our 2011 real GDP growth forecast of 4.6%. Our 2012 GDP growth forecast remains unchanged at 4.8%.

Fiscal boost ahead of the next general election?

With revenues coming in much higher than budgeted this year as well as the backloading of the planned expenditure, the government has room to boost spending in the next few quarters. The

government spent RM154bn in the first three quarters of the year. Its revised 2011 budget suggests that it plans to spend another RM76.8bn (9% of GDP) in Q4, which is 20% yoy more than it spent in Q4 last year. Moreover, in its 2012 budget, the government announced one-off cash transfers to the poor, bonus payments and pay rises for civil servants, as well as various tax exemptions. Most of these are scheduled to happen in early 2012, which should provide a boost to sentiment and private consumption. The ‘people friendly’ budget suggests that the general election, which needs to be held by March 2013, might be near. We expect the government to continue to pump prime the economy before the next general election.

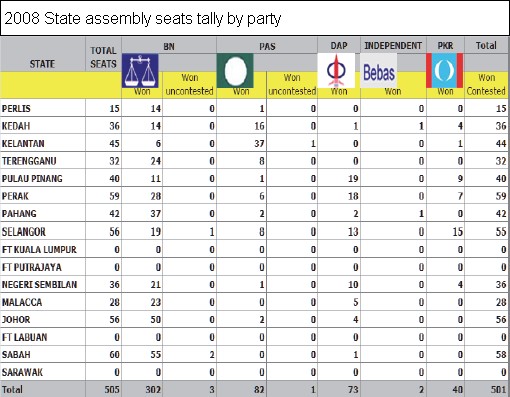

The result of the general election will determine the prospects for structural reforms. The government announced in the budget speech that it will liberalize another 17 services sub-sectors in 2012, including medical, architectural, engineering, accounting, legal, education and telecommunications services. However, there has been no news on subsidy reform or the goods and services tax. We think Malaysia has made some progress in its reforms, as reflected in improved rankings in the global competitiveness index (calculated by the World Economic Forum) and ease of doing business survey (published by the World Bank). However, the less popular reforms have been postponed and appear unlikely to happen before the general election. Its ranking on Transparency International’s Corruption Perceptions Index has also slipped in recent years. Our base case scenario is that Prime Minister Najib will win the general election, but fall short of regaining the two-thirds majority lost in the last general election. The quality of the win will determine whether Najib will stay as prime minister and gain

enough support to push through further changes, in our view.

Monetary policy to stay defensive

With risks surrounding the euro zone remaining high and inflation likely to fall below 3% yoy in Q1 2012, we think BNM will remain data dependent and be ready to cut the policy rate if needed. Our forecast suggests BNM will keep the policy rate on hold until end-2012. However, if the global growth outlook deteriorates in the coming months, we think BNM has both the scope and willingness to cut the policy rate. Similarly, we think the ringgit will continue to trade in line with its regional peers in the near term. However, we think BNM might allow some ringgit out-performance if and when the euro zone situation stabilizes, given that Malaysia’s current account surplus remains strong, domestic demand resilient, and there are signs of pick-up in US economic activity. Domestically, the election result should also be an important determinant of capital flows. A poor outcome for the ruling party could lead to heightened political uncertainty and capital outflows.

Source: Credit Suisse